Pricing is extremely impactful. For many products and for many consumers price is a key feature. Price changes have immediate impact and prices are in many cases very visible. Competitors can react quickly to price changes. Price is the only element in marketing mix that has a direct impact on revenues.

R = P x Q

How to increase price without being noticed?

- Increasing the size of packaging while decreasing the size of its contents.

Price Image

- Nominal prices are quick to change

- Price image is so much harder to change

Price image is connected to all of the elements of the marketing mix and it must be aligned to the firm’s strategic choices of positioning and value proposition.

Odd endings – one way to communicate price image is price itself. The odd-ending price (£0.79 or 379.93) signals that the price is low. However, as the number of items in the catalogue of products priced this way increases, the effectiveness of odd-ended pricing diminishes.

Cost Plus Pricing

Price = (1+m) x (Average Cost)

where ‘m’ is markup (not to be confused with margins)

‘Average Cost’ = variable cost plus allocated fixed costs

Argument for Cost Plus Pricing

Simplicity – an easy to manage pricing method. Practical where thousands of prices must be set repeatedly. It is also easy justifiable and is usually based ‘hard’ cost data which managers usually feel they know well. At corporate level this kind of pricing strategy is usually easy to sell to top management.

Argument against Cost Plus Pricing

Unit or average cost varies with price. Price changes volume and volume than changes average cost. With cost plus pricing market and demand conditions seem to be irrelevant. Average costs are not taken in consideration. Pricing decisions should never be based on costs that are truly fixed costs (short vs. long run costs).

Types of Costs to Consider in Pricing

- Incremental Costs – are costs that rise and fall when prices change. This has an effect on the relative profitability.

- Variable Costs – these are costs of raw materials in manufacturing process. Most fundamentally these are the basis costs of doing business.

- Fixed Costs – these costs are not affected by the output levels (how much the company actually sells). These are the costs of being in business.

- Avoidable Costs – are the only costs relevant to pricing. These are the costs which not yest been incurred or can be reversed. Usually they include the cost of selling the product, delivering it to customers and replacing the sold item in inventory).

- Sunk Costs – these include past expenditure on research and development and any other costs which cannot be changed regardless of decision made at present.

The issues with incremental and sunk costs are become apparent at the time when a business is exposed to seasonal demand fluctuations (highly variable demand), business capacity management, high fixed costs to serve peaks in demand and unused installed capacity. Managers must always consider the appropriate costs for pricing, time frame and never ignore potential competitive pressures. Never forget about your cost when setting prices, study them carefully and try to guess how low the prices of your competitors can be.

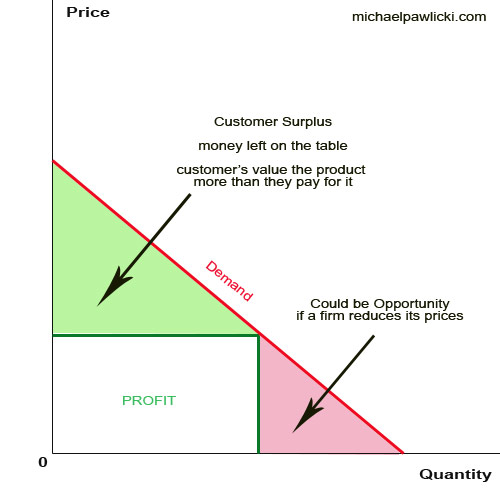

Tracing Complete Demand Curve

- It needs sophisticated methods. Questioning the consumer directly might be very unreliable and difficult)